Debt can be a heavy burden on anyone’s life, both financially and emotionally. This often leaves individuals feeling hopeless and having a bad relationship with money. However, if there’s a will, there’s a way.

Here, we cover several lies about debt, including some tips from finance expert Dave Ramsey. Use this list to avoid them at all costs and to improve your relationship with money. If done right, you can live a happy life where money enhances it.

1. Debt Is Normal

Unfortunately, most people believe that having some debt is normal. In fact, according to Dave Ramsey, “1 in 5 Americans have fallen deeper into debt since June of 2022.” Just because something is normal doesn’t make it right. People fall into debt for many reasons. However, none of these reasons make it right in the long term.

2. You Have Plenty of Time

It’s great to be optimistic about your future, but no one has plenty of time for anything. The truth is, we are all lucky each day we are alive. Everyone is one illness or accident away from having limited time. Still, don’t panic if you have debt.

Instead, create clear financial goals and deadlines. Aim to pay off as much debt as you can each month while not accumulating any more.

3. All Debt Is Bad

Unless you have hundreds of thousands of dollars stored somewhere, you’ll take out a loan at some point. However, not all debt is created equal. For example, buying a house to live in or generate passive income isn’t bad debt.

You can purchase a home with a comfortable monthly mortgage payment. If you’re ambitious, you can buy a second home after a few years and have tenants pay it off for you.

4. You Don’t Earn Enough

Believe it or not, there are stories of people who’ve paid off their mortgage with a teacher’s salary. This means the excuse that you don’t earn enough to get out of debt might be invalid. Do an honest evaluation of your spending and note which expenses you can trim.

Focus on the largest ones first. A mortgage is most people’s most significant expense and the hardest to eliminate. For example, downsizing your home takes a lot of effort and humility, but the upside is living debt-free. Additionally, you can refinance your loan if you currently pay high interest.

5. Debt Isn’t That Bad

Whoever says that carrying debt isn’t bad has likely never been debt-free. Although you shouldn’t live pessimistically, avoid living in debt. Take the time to understand how much debt you carry and set a deadline to pay it off. This alone will at least give you a glimpse of it during the early stages of your debt-payoff journey.

6. A Budget Limits Your Freedom

Budgets aren’t fun for most people. If done incorrectly, they cause stress and do little to move you closer to your financial goals. However, a proper budget will keep you out of debt and allow you to build wealth.

This will vary according to your style, but a simple spreadsheet is all you need. However, if you want to utilize technology, there are many free apps to help you create a budget.

7. You Need to Keep up With the Joneses

Most of the time, people purchase things to impress others. For example, many people purchase expensive vehicles to show them off to family and friends. However, keeping up with your friends and family comes at a heavy cost and is not worth it.

Is constantly worrying about how you’ll make ends meet worth driving a luxury vehicle? Most would argue no. Replace luxury vehicles with whatever you’re currently accumulating debt for.

8. Buying Now Is Necessary

Whether you discover the latest smartphone or gadget on TikTok, the impulse to purchase it right this second is high. FOMO (fear of missing out) kicks in, and many purchase these items with their credit card.

If you don’t have the money to purchase an item, avoid using your credit card. In fact, it may be best to close all your credit cards except one.

9. Not Using Debt Is Hard

Not relying on your credit card to make purchases is hard. However, the secret to making this easy is to make this a habit. With a proper budget, you can pay off your credit card each month and avoid racking up more debt.

10. You Don’t Need Your Spouse to Agree

Whether you like it or not, you and your spouse must be on board with most things, including your finances. Misalignment with your spouse increases the odds of a divorce and builds debt. Think about it: If one of you is careless with spending and the other isn’t, you’re still racking up debt.

You and your spouse will probably share bank accounts and even income. Thomas Stanley, the author of The New York Times bestseller The Millionaire Next Door, was right that choosing the right spouse is one of the leading factors in building wealth.

11. You Need a Credit Card for Emergencies

It’s wise to save three to six months of your living expenses. This way, you have disposable income you can use during emergencies. Although having a credit card with a high limit may give you the illusion that you’ve prepared for emergencies, think again.

Credit cards often carry a high interest rate. If you only make the minimum payment, you’ll pay much more than you borrowed.

12. Living Debt Free Isn’t Possible

Feeling hopeless in the early stages of the debt-paying process is normal. However, living with debt forever doesn’t have to be your reality. If people with low salaries have climbed out of debt, so can you.

Instead of focusing on what you don’t have, focus on your strengths. For example, if you have a high salary, focus on making large payments toward your debt. If you have a low income but have extra downtime during the week, drive Uber to pay off your debt faster.

13. Minimum Payments Are Enough

Making the minimum payment towards debt is never smart. Consider that if you were to pay the minimum fee for a $2,000 balance, you’d end up paying more than double this amount. This is why it’s better to make all of your purchases in cash to position yourself to pay off your credit card each month. Even better, only use cash if you find yourself constantly racking up unnecessary debt with your credit card.

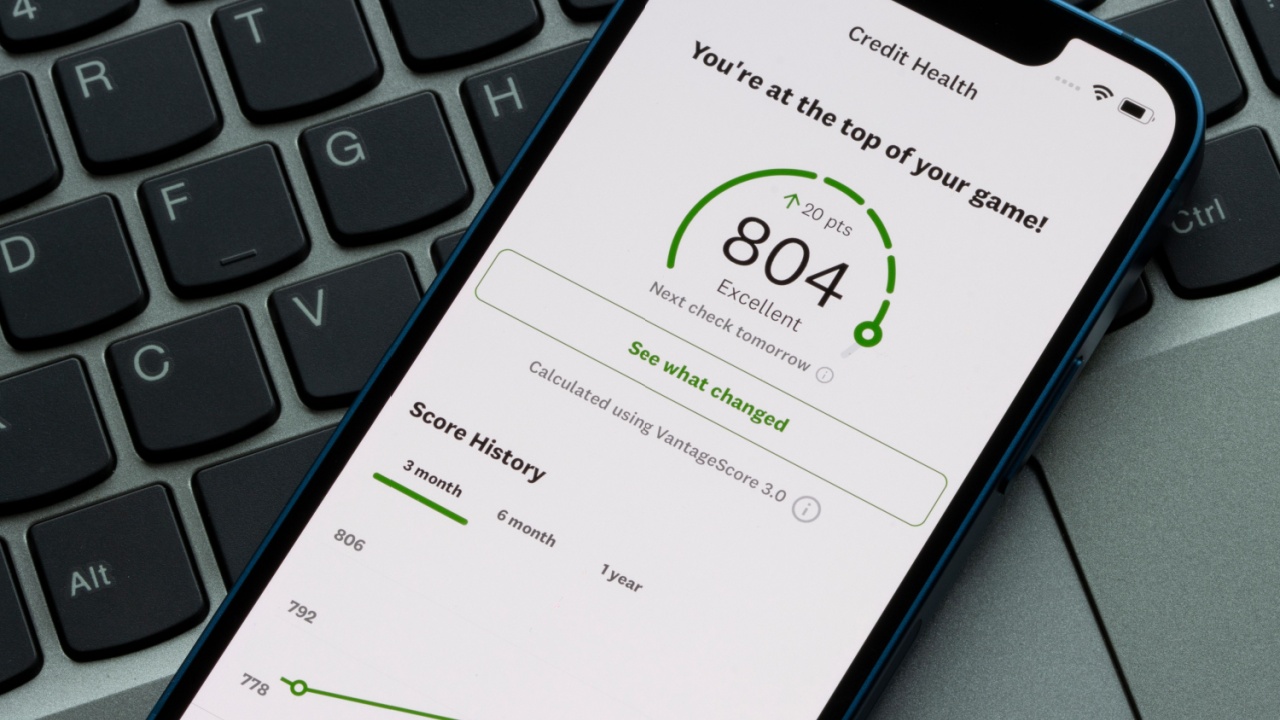

14. You Need Debt to Build Credit

It’s true that you need a history of responsibly making timely payments to build your credit score. However, you don’t need to rack up debt. Instead of letting a balance revolve after your credit card billing cycle, pay it off before the end of each cycle. This way, you have a record of paying off debt without paying interest each month.

15. Debt Consolidation Saves Money

Consolidating all your debt into a single loan can be smart, but only when done correctly. For example, it’s not wise if the initial transfer and interest fees are high enough to increase your overall balance.

Simply put, debt consolidation should make your monthly payments easier since you’ll pay off one loan versus two or five. Additionally, many credit cards offer a year of no interest, which will help you save money if you pay off your balance before the promo expires.